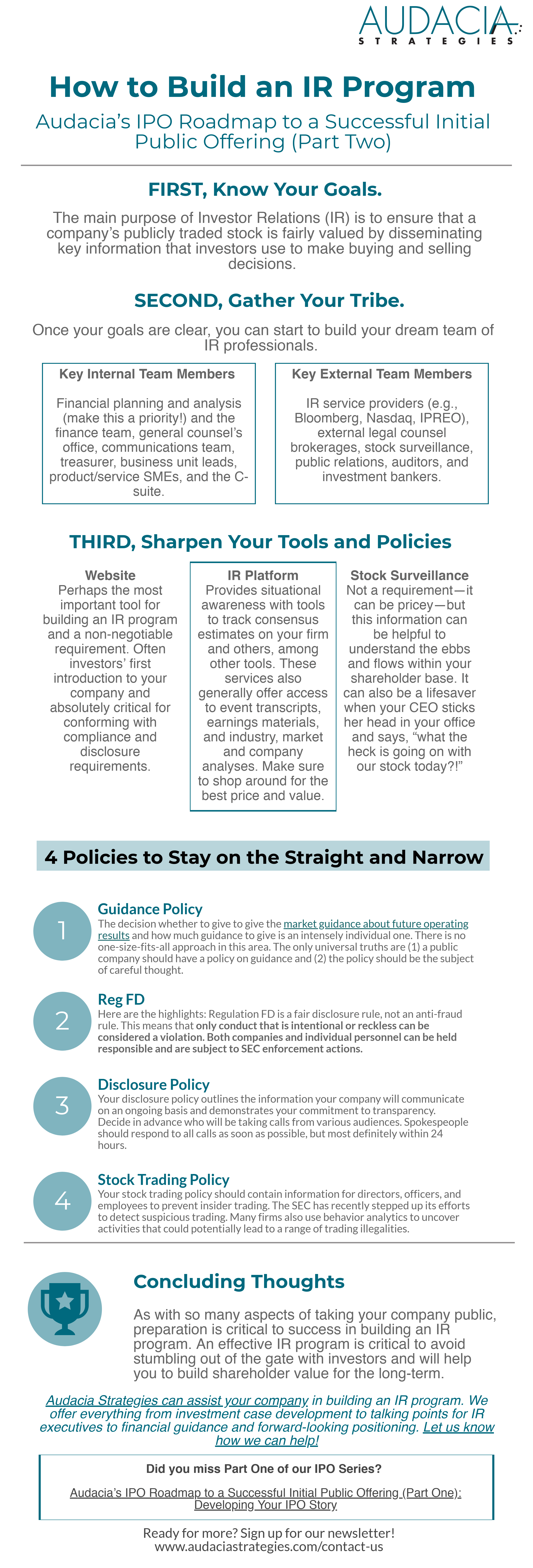

Over 70% of M&A Deals Fail to Meet Their Goals — Beat the Odds With These 5 tips

The last time we talked about M&A deals here on the blog, we were all wondering how the pandemic would affect the economy and watching some of the biggest players abandon deals in the pipeline or take the Covid chaos as an opportunity to get into the game.

While the pace of recovery has varied among companies and sectors in 2021, U.S. deal volume and value are up from 2020 numbers and forecasted to continue to rise. Meanwhile global mergers and acquisitions for the first half of the year totaled a record $2.4 trillion, up 158% for the same period last year.

But even as the numbers continue to rise and many organizations sharpen their knives, M&A deals have also gotten more complicated. Let’s look at the why and how these changes should influence your approach to due diligence.

3 Major Changes Afoot

In recent years, M&A has become something akin to 3-dimensional chess (if players could constantly enter and exit and the rules were also a moving target). Three major changes contribute to the increasing complexity.

1. COVID-19 has hastened disruptive trends.

First, COVID-19 has hastened pre-existing disruptive trends across industries, drawing a clear bright line between business models that will succeed in the future and those that are outmoded. Rather than looking merely to deals that will create scale and cost synergies within an industry, organizations are looking to increase scope and add new capabilities, especially in technology, proprietary data, or scarce talent.

2. The M&A process is faster and more complex.

Second, the M&A process has become faster and more complex. Whereas corporate acquirers have always had the upper hand with deeper pockets and M&A deal experts to lean on, private equity players are giving them a run for their money. Nearly every deal is now an auction. Access to debt capital has been a nonissue during this crisis, so competition for attractive, high-growth assets is higher than ever.

Add to this mix access to data, broadening regulatory scrutiny of deals on the basis of national interest, and a flood of major technology companies. Consider, for example, the involvement of Amnesty International in the Google, Fitbit deal. The organization sent a letter to E.U. regulators, arguing that they should block the deal unless Google addresses human rights issues like the right to privacy and nondiscrimination. Evaluating the environmental, social, and governance (ESG) impact is becoming an integral part of the diligence process. For many looking to make a deal, this is new territory.

3. COVID-19 has forced organizations to adapt their M&A deals.

Finally, COVID-19 has forced organizations to adapt quickly in a myriad of ways and M&A is no exception. In a 2020 Bain & Company survey of M&A practitioners, 70% of respondents reported that diligence was more challenging during the pandemic and 50% found it harder to close deals. Companies that adapted quickly, developing capabilities in virtual diligence and virtual integration, have made great strides.

The use of data in the M&A process is another differentiating factor. Smart M&A teams are leveraging data (and sometimes artificial intelligence) to screen for targets and create profiles, so they are ready even before targets come to market. During diligence, companies are using digital platforms to perform risk analysis and generate customer insights among other data collection to give themselves an edge.

As companies rewrite their M&A strategies for a post-pandemic world, some of the principles of what a good deal looks like still hold true. The most astute M&A teams understand the importance of proper planning and forethought in the months, weeks, and days before an acquisition. And they understand that due diligence goes well beyond the financials.

Beyond Financial Due Diligence

Given the above changes and the likelihood that M&A will continue to play an increasing role in revenue growth for years to come, it pays for leaders to get clear about their own approach to due diligence. In particular, it’s critical for organizations not to overlook the non-financial aspects of due diligence.

Now, don’t get me wrong. We aren’t trying to downplay the importance of financial due diligence. You need to run the numbers and they absolutely need to make sense. Still, all too often it’s non-financial factors that we see tripping up M&A deals.

By non-financial due diligence, we have in mind:

- Is this merger the right cultural fit for your organization? And, do you have a strategy for cultural integration once the deal closes?

- Do you have a solid, agile, proactive M&A team in place and ready to jump into action when the right deal opportunity comes along?

- Is this deal really the right deal showing up at the right time or are you suffering from deal fever?

- Have you considered the intangibles? Here I mean variables like corporate reputation, brand promise, employee sentiment, and customer engagement?

What can you do to position your organization for future M&A success?

We see five things leaders can do to equip their organizations for future M&A success:

Re-evaluate how M&A fits into your broader business strategy. As your business model shifts and you revise your corporate strategy, you will also need to update your M&A team’s goals. How has the pandemic affected your industry and sector? Does this change where to buy vs. build to remain competitive?

Consider non-traditional M&A. One of the ways in which M&A is changing is that companies are getting creative. Many are using a combination of joint ventures (JV’s), partnerships (with or without equity, with or without financial sponsorship), and corporate venture capital to tailor deals and integration. Also, organizations are partnering with other companies to explore opportunities for mergers and acquisitions. This lowers the risk and increases the likelihood of selecting the right deal.

Bring expertise into the process early. Given the growth in speed, scope, and capability deals, specialized expertise early on can help organizations better gauge fit. When you work with an external team like Audacia Strategies during the diligence process or even before, you get a set of eyes and ears in the room as an extra “gut check.” We know the transaction cycles, value creation opportunities — and how to avoid the trapdoors.

Know the lay of the land and be ready to spring into action. The fierce competition for deals means that firms can no longer wait for bankers to come to them or rely on a singular source of deal intelligence. Companies need to continually scan the industry landscape, see how it’s evolving, and be ready to focus when an opportunity arises. Establish an ecosystem of external partners (bankers, tax and legal advisors, private equity experts, due diligence partners, etc.) who have access to data, connections, and can strike quickly.

Go beyond financial due diligence. When it comes to increasing capacity through an M&A deal, it’s not sufficient to simply understand the value of a target. You also need to assess factors like cultural fit, sustainability, and employee and consumer sentiment at the diligence stage. Consider also regulations and new challenges that may arise as your organization evolves.

The future of M&A is here. If you’ve been sitting on the sidelines, now is as good a time as ever to jump into the fray. The above will give you some orientation, but if you really want to ensure your deal goes smoothly, you need the right partners on your bench. At Audacia, we’re here to walk you through the non-financial side of due diligence. Contact us to talk about your M&A strategy.

Photo credit and description: Group of people working around a laptop at an office by Flamingo Images from NounProject.com