Audacia’s IPO Roadmap to a Successful Initial Public Offering (Part Two): How to Build an IR Program

A successful initial public offering requires syncing up several moving parts. If doing a product launch feels like playing “Twinkle Twinkle Little Star,” an IPO feels like playing “Beethoven’s 9th.” Of course, to play a symphony, you need an orchestra. For your successful IPO, that means building an IR program.

If you missed Part One, we discussed how to develop your IPO story. Once you have your story, it’s time to get operational. So, this week we’ll look at answers to the following questions:

How do you structure your IR program?

Who are the key partners and players?

What are the key tools and policies that will set you up for success?

Without further ado, let’s talk building an IR program.

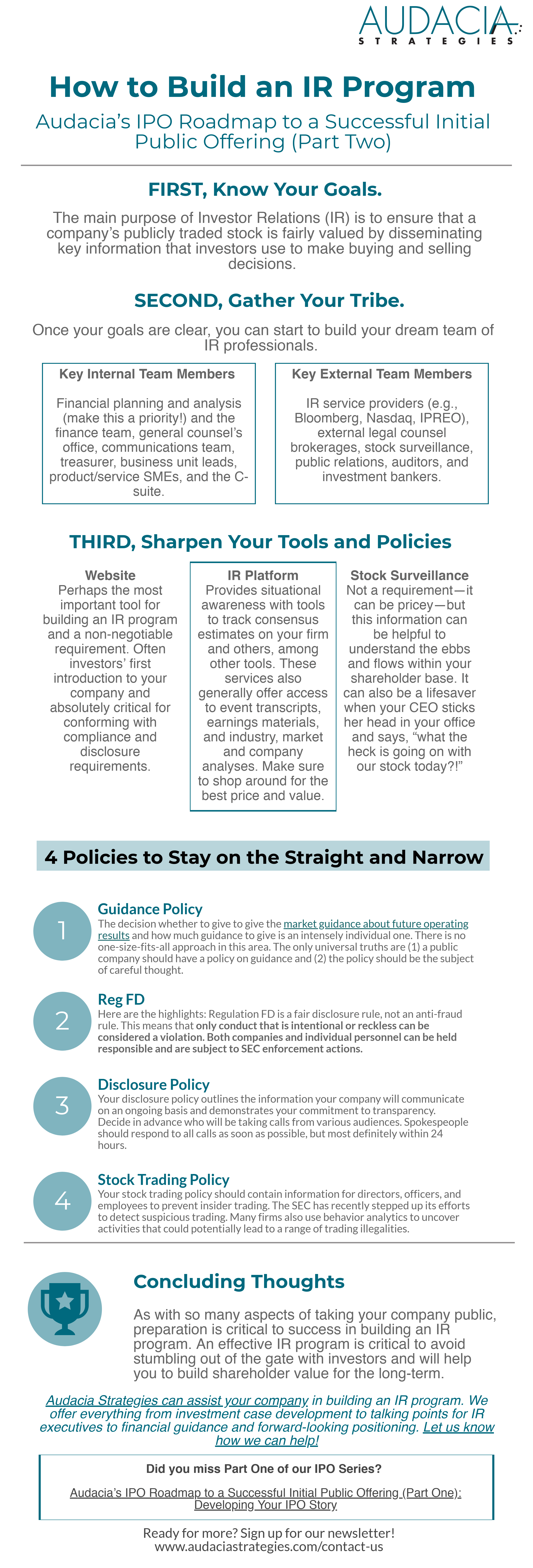

First, Know Your Goals.

We’ve discussed what IR is and isn’t before. The main purpose of IR is to ensure a company’s publicly traded stock is fairly valued by disseminating key information that investors use to make smart buying and selling decisions. IR departments communicate with investors (obviously), research analysts, regulatory and oversight organizations, customers, suppliers, media, and the broader financial community.

A solid investor relations plan will help guide your IPO discussions and ease your transition to a public company. The most important job? Establishing and building corporate credibility with your stakeholders through transparent and consistent communication.

A solid investor relations plan will help guide your IPO discussions and ease your transition to a public company. The most important job? Establishing and building corporate credibility with your stakeholders through transparent and consistent communication.

Second, Gather Your Tribe.

Once your goals are clear, you can start to build your dream team of IR professionals. Hopefully, you have established and maintained strong business relationships over the years. Don’t be shy about calling on these contacts now.

Consult the following key partners and players:

Internal relationships: financial planning and analysis (make this a priority!) and finance team, general counsel’s office, external legal counsel, communications team, treasurer, business unit leads, product/service SMEs, and the C-suite.

External Relationships: service providers (Bloomberg, Nasdaq, IPREO, etc.), brokerages (JPMorgan, Jeffries, Goldman Sachs, etc.), stock surveillance (if using), public relations (if using and partnered with your internal communications team), your audit team (e.g., Deloitte, PWC, E&Y, etc.), and investment bankers.

Tools for Building an IR Program

We cover the basics below. Although we could get into using CRM systems, integrated blast email services, etc., for today, let’s keep it simple. Shall we?

Website: Your IR website is perhaps the most important tool for building an IR program and a non-negotiable requirement. Not only is your IR website often investors’ first introduction to your company and a perfect vehicle for disseminating your investment story, it’s also absolutely critical for conforming with compliance and disclosure requirements. I could go on about websites and their importance—a topic for another day!

Here are key recommendations to keep in mind for your IR website:

-

- Make investor content easy to access—consider the user experience when designing your site.

- Provide content that accurately describes your compelling investment thesis.

- Keep the most requested information easy to find and download, i.e., earnings materials, investor presentations, etc.

- Make contact information readily available. If you plan to be active on social media, include those links as well.

- Make it mobile responsive—always good website etiquette!

- Include governance information—officer and director information, committee charters and ethics documents, committee memberships, etc.

- Keep a running list of company news/press releases.

- Ensure that data feeds from the SEC and streaming stock quotes are accurate and timely.

IR platform: This type of tool will help to track consensus estimates on your firm and others, trading patterns, analyze your shareholder base, research and target new investors, review ownership trends, etc. These services also generally offer access to event transcripts, earnings materials, and industry, market and company analyses.

Many providers offer this type of service at varying price points. So, shop around. To operate efficiently and quickly it’s important to have situational awareness of your firm’s position among peers and within the market. These tools help you to track just that.

- Examples include: Nasdaq, IPREO, Bloomberg, and others.

Stock Surveillance: While not a requirement—it can be pricey—this type of information can be incredibly helpful to understand the ebbs and flows within your shareholder base. It can also be a lifesaver when your CEO sticks her head in your office and says, “what the heck is going on with our stock today?!”

Stock surveillance is a service that focuses on tracking and analyzing movement in your company’s institutional shareholder base. Service providers will use a combination of publicly available data as well as proprietary and research-based methodologies and technologies.

There is a mix of art and science in this tool. It can be controversial, but I’ve found it to be very helpful in providing situational awareness. It is particularly important during times of crisis (market or company).

Key Policies for Staying on the Straight and Narrow

Every public company must decide whether and to what extent to give the market guidance about future operating results. The decision whether to give guidance and how much guidance to give is an intensely individual one. There is no one-size-fits-all approach in this area. The only universal truths are (1) a public company should have a policy on guidance and (2) the policy should be the subject of careful thought. As you continue building an IR program, keep the following policies in mind.

1. Reg FD

We’ve discussed Reg FD policy a few times. Specifically see:

Here are the highlights: Regulation FD is a fair disclosure rule, not an anti-fraud rule. This means that only conduct that is intentional or reckless can be considered a violation. Both companies and individual personnel can be held responsible and are subject to SEC enforcement actions.

Such enforcement actions can include injunctions, fines, and obligations to disclose the violation.

For more information about Reg FD and the SEC’s enforcement of the law, check out this list of frequently asked questions. But always remember that nothing you read online, including this article, is a substitute for qualified legal counsel.

2. Disclosure Policy

Your disclosure policy outlines the information your company will communicate on an ongoing basis and demonstrates your commitment to transparency. Avoid making the policy too narrow. It could come back to bite you during any potential litigation. Decide in advance who will be taking calls from various audiences. Spokespeople should respond to all calls as soon as possible, but most definitely within 24 hours.

This policy generally designates company spokespersons, approved channels of disclosure (website, SEC filings, social media, if your firm chooses to do so), handling of earnings and forward-looking guidance, and quiet periods.

A note on quiet periods:

The purpose of a quiet period is for a public company to avoid making comments about information that could cause investors to change their position on the company’s stock. There are no official guidelines on quiet periods. Practices vary by company requirement—for example, a Mega-cap firm that is part of the Dow may consider its quiet period to begin 2 weeks before the end of the fiscal quarter and conclude with their earnings report after quarter close.

However, a small-cap firm that is lightly covered may need to continue to take calls—even if they cannot answer some of the investor questions. In general, during a quiet period most companies either (a) allow no formal or informal communications at all (AKA all calls go to voicemail) or (b) allow limited communication and interaction with investors/analysts by:

- Answering only fact-based inquiries

- Sharing information only on overall long-term business and market trends

- Announcing if it expects financial results to differ materially from earlier forecasts

Again, it’s hard to generalize here. Having a policy tailored to your IPO ensures that everyone knows the plan and has a common starting point.

3. Stock Trading Policy

The SEC has recently stepped up its efforts to detect suspicious trading. Sophisticated data analysis tools track shady patterns such as “improbably” successful trading across different securities over time. Many firms also make use of behavior analytics to uncover activities that could potentially lead to a range of trading illegalities.

Your stock trading policy should contain information for directors, officers, and employees to prevent insider trading. This article contains a list of best practices from someone charged with and convicted of insider trading. Hindsight is 20/20, right?

Concluding Thoughts

As with so many aspects of taking your company public, preparation is critical to success in building an IR program. So make sure that you have positioned your company to be successful in IR. An effective IR program will be critical to avoid stumbling out of the gate with investors and will help you to build shareholder value for the long-term.

Audacia Strategies can assist your company in building an IR program. We offer everything from investment case development to talking points for IR executives to financial guidance and forward-looking positioning. Let us know how we can help!

Next up: Congrats! You’re Public. Now What?

Photo credit: Andriy Popov