Breaking Down Mid-Year Earnings Reports—What Investors and Analysts Expect

We have just crossed the mid-year point in the world of stocks, bonds, and financial markets. Q2 is officially in the bag! That means most firms are busily preparing and reporting their mid-year earnings reports (10-Qs), while many investors are anxiously waiting with bated breath.

Because 71% of publicly traded companies follow a calendar fiscal year (outliers include Apple and the US Federal Government (YE Sept 30), FedEx (YE May 31), and Microsoft (YE June 30)), investors and analysts look extra closely at earnings reports this time of year. And for good reason—mid-year earnings reports can be the key to assessing a company’s full year outlook.

So, let’s talk about what you should keep in mind as you check out your peers’ mid-year earnings reports and prepare your own.

Mid-year Earnings Reports and Expectations

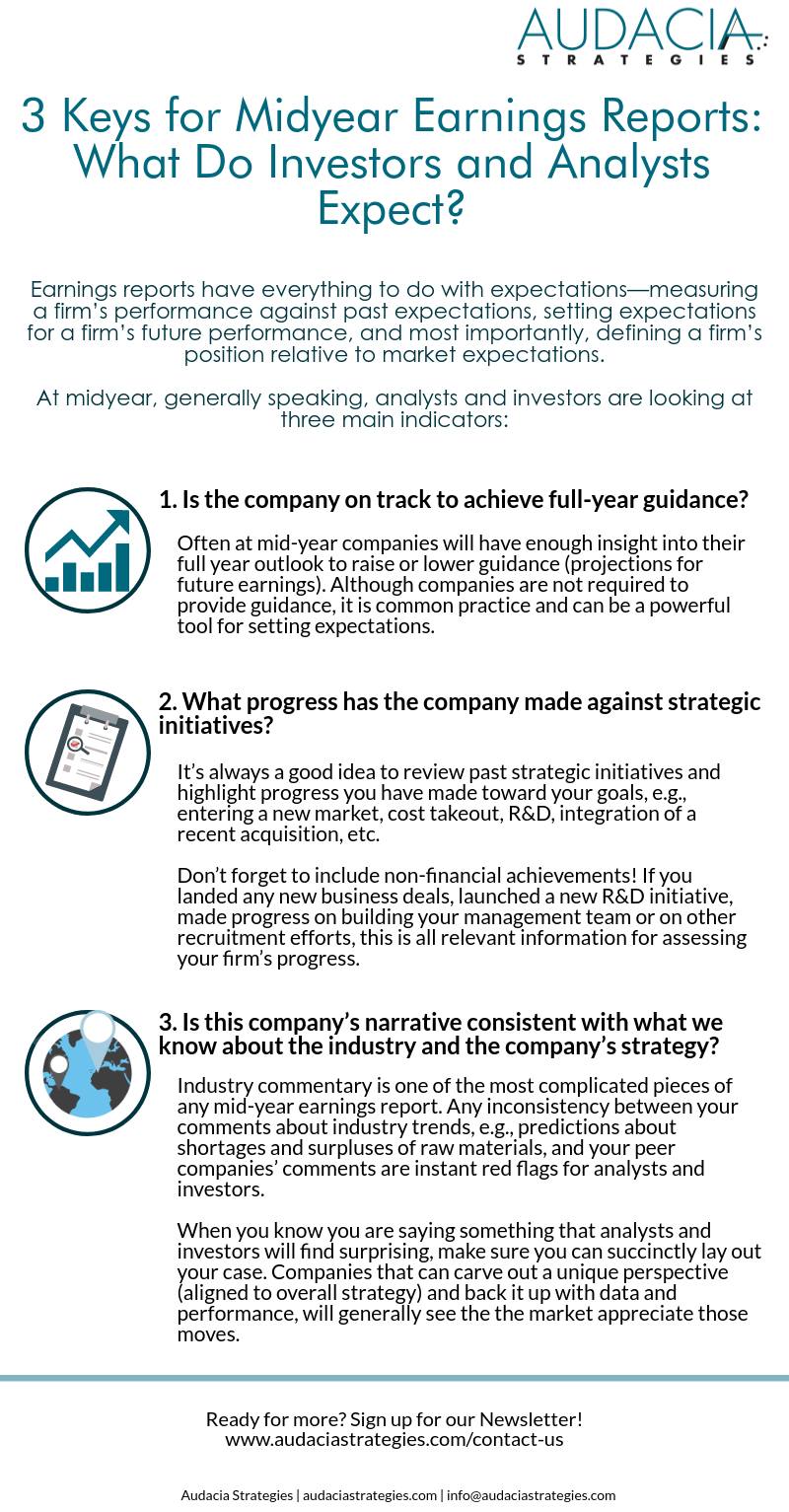

Earnings reports have everything to do with expectations—measuring a firm’s performance against past expectations, setting expectations for a firm’s future performance, and most importantly, defining a firm’s position relative to market expectations.

The skill with which you communicate these specifics can affect analysts’ valuation of a firm, which in turn affects investor perceptions.

As Gerald Loeb (founding partner of E.F. Hutton & Co., a Wall Street trader and brokerage firm) put it so well, “stocks are bought on expectations, not facts.” This is true. But, as we also know, expectations depend on facts. So let’s look at the facts that are most relevant.

(Not) Just the Facts

What’s essential to communicating mid-year earnings reports is to paint the best possible picture, given the available facts. But what does painting the best possible picture mean in this context? It means evaluating Q1 and Q2 against the major milestones laid out in your 2016 strategic plan and making the best case, true to your numbers, for seeing continued momentum in Q3, Q4, and beyond.

At midyear, generally speaking, analysts and investors are looking at three main indicators:

1. Is the company on track to make full-year guidance?

Often at mid-year companies will have enough insight into their full year outlook to raise or lower guidance (projections for future earnings). Although companies are not required to provide guidance, it is common practice and can be a powerful tool for setting expectations. But the decision about whether to give guidance and how much is an individual one.

Factors to consider when it comes to guidance:

- Primary Liability: Several provisions in the federal securities laws can create liability for forward-looking statements. For example, Section 11 and 12 of the Securities Act of 1933 impose liability on issuers, their officers and directors, and underwriters for misstatements or omissions of material facts. Because of the potential legal issues here, it’s important for those giving guidance to speak carefully, completely, and deliberately.

- Safe Harbors: The Private Securities Litigation Reform Act (PSLRA) of 1995 enacted safe harbor provisions for forward-looking statements that are identified as such and accompanied by “meaningful cautionary statements” that could cause actual earnings to differ from guidance. However, PSLRA safe harbor provisions do not apply to IPOs or enforcement proceedings brought by the SEC.

- Regulation FD: The prohibition on selective disclosure of material nonpublic information should also be taken into account in any discussion about whether to provide or update guidance. Guiding analysts about future earnings is permissible under Regulation FD, as long as the general public is informed at the same time.

This article from a Harvard Law School forum offers a more detailed overview of what public companies should know about giving guidance. Keep in mind, though, that there’s no substitute for consulting the pros when it comes to navigating the choppy waters of when to provide guidance and when to raise or lower these expectations.

2. What progress has the firm made against strategic initiatives?

If you are presenting mid-year earnings reports during a call with investors, it’s always a good idea to start with an overview of past strategic initiatives and whatever progress you have made toward your goals, e.g., entering a new market, cost takeout, R&D, integration of a recent acquisition, etc.

In going over the details of your progress, be as specific and transparent as possible. Analysts and investors like to hear specific examples backing-up statistical claims. So if you claim, for instance, that revenues for a certain sector grew 6% in Q2, be sure to talk about what exactly impacted earnings. Did a new licensing deal pan out? Was a particular marketing approach successful? Did you hire a fresh, young whiz kid who is setting the world on fire?

Point out opportunities for capitalizing on the momentum you’re building and places where it would be prudent to pull back temporarily or long-term. Be candid about any milestones or strategic initiatives that were less than successful too. As a favorite former boss used to say, “Don’t take it on the chin.” Rather, put the challenges in context and talk about what you’re doing to correct course or why you expect industry trends to shift. Not every initiative works. Real talk from your executives can go a long way in building trust over time.

Don’t forget to include non-financial achievements here as well. If you landed any new business deals, signed any new clients, launched a new R&D initiative, made progress on building your management team or on other recruitment efforts, this is all relevant information for assessing your firm’s progress. Remember to drive your points home by reiterating your key takeaways at the end of this section.

3. Is this company’s narrative consistent with what we know about the industry and the company’s strategy?

Industry commentary is one of the most complicated pieces of any mid-year earnings report. Any inconsistency between your comments about industry trends, e.g., predictions about shortages and surpluses of raw materials, and your peer companies’ comments are instant red flags for analysts and investors.

Outlier comments will be pressed during Q&A. This could be a good thing, if used strategically. Taking a novel view of your market or industry could indicate a key differentiator in market approach, which could be indicative of future earnings outperforming guidance (investors are always looking to capture alpha!). So, it literally pays to be prepared.

However, if your commentary goes against conventional wisdom or contradicts previously discussed strategic goals (i.e., your investment case), it will get more questions and be met with skepticism—guaranteed. When you know you are saying something that analysts and investors will find surprising, make sure you can succinctly lay out your case. Companies that can carve out a unique perspective (aligned to overall strategy) and back it up with data and performance, will generally see the the market appreciate those moves.

All the above barely scratches the surface and there is a lot more that could be said about each of these indicators. But, of course, the most valuable recommendations for preparing mid-year earnings reports are those specific to your firm’s needs and your industry’s trends.

So, if your investor relations strategy is in need of a touch-up, the experts at Audacia would love to help you paint the best possible picture. Contact us today to set up a consultation.

Photo Credit: Dmitriy Shironosov

Leave a Reply

Want to join the discussion?Feel free to contribute!