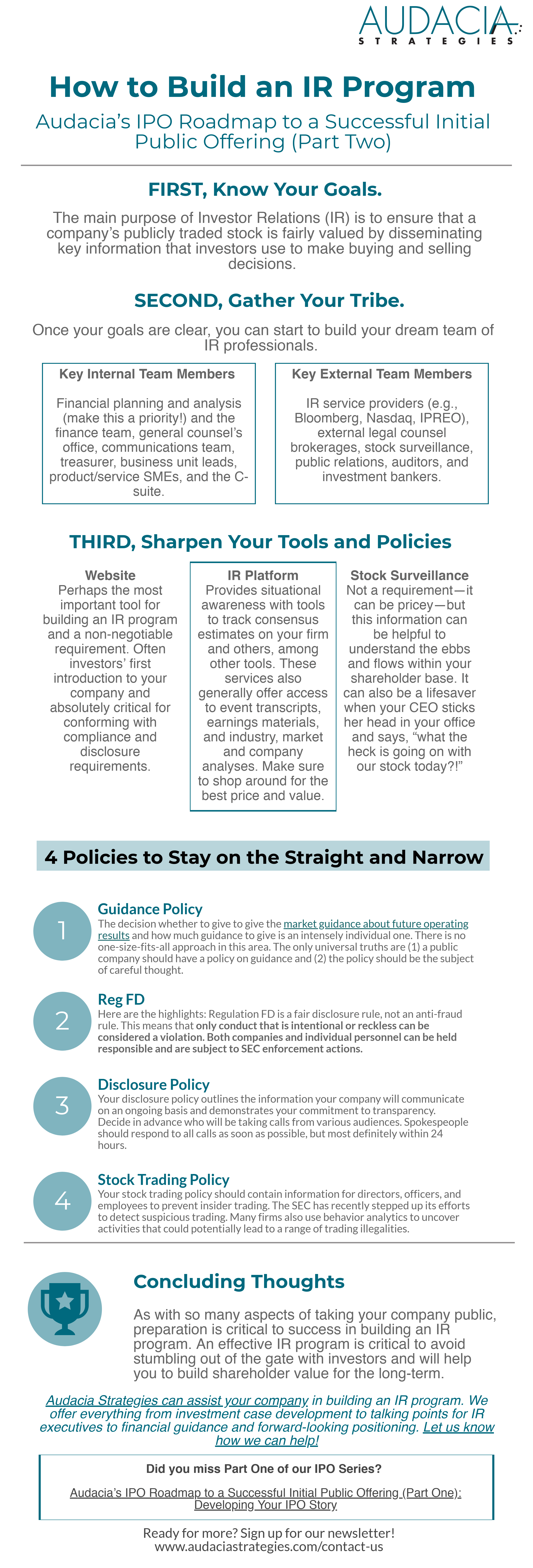

Are Apple and Tesla Using Monopoly Money?—Business Value, Valuation Myths, and Your Business (Part 1 in our series on Business Valuation)

This is the first part of our series on business valuation. Check out part two where we dig into what influences these different types of valuation.

Business valuation is making headlines these days. With the announcement that Apple is the first publicly traded company to surpass the trillion dollar mark and Elon Musk making Twitter waves about taking Tesla private putting its value at $72 billion, it can feel like some of the big dogs get to play with Monopoly money.

Adding to this perception that business valuation isn’t always (completely) based in reality (hint: there is a big difference between what a company’s worth in “real money” vs. what it could be worth in an acquisition), consider what’s happening in the Venture Capital (VC) ecosystem. VC investors love to reward growth metrics with higher valuations. So it’s common for startups to shop VC firms looking for the best price. This practice has some experts worried that the VC industry is the next bubble.

However, before we throw our hands up, let’s look at what we know about types of business valuation and what these mean for successful non-unicorns and their investors.

Public vs. Private Company Valuation

- Apple reaches $1,000,000,000,000 value (CNN Money, 8/2/18)

- Elon Musk Might Take Tesla Private in a Move That Values the Company at $82 Billion (Time, 8/7/18)

- Slack Raises $427 Million More, at $7.1 Billion Valuation (NYTimes, 8/21/18)

One of these things is not like the other.

The first thing to understand about business valuation is that we can’t easily compare the values of publicly and privately held companies. Determining the market value of a company that trades on a stock exchange (e.g., Apple, Tesla, Facebook) is fairly straightforward (though we’ll see below that this method doesn’t take into account all types of value investors might want to consider).

However, for private companies, the process is not as straightforward or transparent. This is because unlike public companies that must adhere to the SEC accounting and reporting standards, private companies do not report their financials publicly and since they aren’t listed on the stock exchange, it’s more difficult to determine a value for a private company.

However, for private companies, the process is not as straightforward or transparent. This is because unlike public companies that must adhere to the SEC accounting and reporting standards, private companies do not report their financials publicly and since they aren’t listed on the stock exchange, it’s more difficult to determine a value for a private company.

Public company valuation: generally in the press you see market capitalization (AKA market cap, in slang) used as a valuation description (see: Apple, Tesla).

- Market cap = stock price x number of outstanding shares

- Example: Apple shares outstanding: 4,829,926,000 x $219.01 (closing price on 8/27/18) = $1.06T

This is pretty simple, but keep in mind that this doesn’t necessarily take into account the full range of measures used to assess the potential purchase price (aka value or market value or valuation) of a business. One of the most commonly used valuation metrics for a public company is enterprise value.

- Enterprise value = a corporation’s market cap (see above) plus preferred stock plus outstanding debt minus cash and cash equivalents found on the balance sheet

So, let’s say that you wanted to buy Apple. The enterprise value is the amount it would cost you to buy every single share of a company’s common and preferred stock, plus take over their outstanding debt. You would subtract the cash balance because once you have acquired complete ownership of the company, the cash is yours.

- Example: Apple’s Enterprise Value

Apple’s market cap: $1.06T + outstanding debt: $114.6B – cash and cash equivalents: $70.97B = 1.1T

Okay, so how do we determine the value of a private company. Here there are several different approaches.

Headline valuation: private company valuation metric generally based on the price paid per share at the latest preferred stock round (i.e., investment round) multiplied by the company’s fully diluted shares (see: Slack).

- “Fully diluted shares” = Common Shares outstanding + Preferred Shares outstanding + Options outstanding + Warrants outstanding + Restricted Shares (RSUs) + Option Pool (sometimes)

See. It’s complicated. And, also a bit of a black box for the average investor. It infers that all shares were acquired at the same price as the latest round, which isn’t typically the case.

Generally, this type of valuation is used because it’s impressive on paper and in the paper (or on the screen). Keep in mind that this basic formula, while it may seem complicated, avoids a lot of the technicalities of private company valuation (but if you’re interested Scott Kupor of Andreessen Horowitz did a great post on VC valuation here).

Although private companies are not usually accessible to the average investor, there are times when private firms need to raise capital and, as a result, need to sell part ownership in the company. For example, private companies might offer employees the opportunity to purchase stock in the company or seek capital from private equity firms.

In these cases, investors can assess business valuation using another common approach:

Comparable company analysis (CCA): a method of business valuation that involves researching publicly traded companies that most closely resemble the private firm under consideration. Such analysis includes companies in the same industry (ideally a direct competitor) and of similar size, age, and growth rate.

Once an industry group of comparable companies has been established, averages of their valuations will be calculated to establish an estimate for the private company’s value. Also, if the target firm operates in an industry that has seen recent acquisitions, corporate mergers, or IPOs, investors can use the financial information from those transactions to calculate a valuation.

Discounted cash flow (DCF) valuation: similar to the above method, this approach involves researching peer publicly traded companies and estimating an appropriate capital structure to apply to the target firm. From here, by discounting the target’s estimated cash flow, investors can establish a fair value for the private firm. A premium may also be added to the business valuation to compensate investors for taking a chance with the private investment.

Misconceptions About a Company’s Worth

So, what’s your company “worth?” If you’re not running a billion or trillion dollar company, you may be wondering where to start in figuring out your company’s valuation. We discussed the basics of business valuation in a previous blog article, which will give you some answers.

And, of course, you may now be wondering whether to take your company public. Or perhaps you’re thinking about raising money to fund your business. You can find out more in Audacia’s IPO Roadmap series (Part One is here).

Now that you know the basics, let’s bust a few common myths:

Business Valuation Myth #1: Valuation is a search for “objective truth.”

This may be obvious already, but all valuations have some bias built-in. Yes, investors will pick and choose the model or approach they want to use. So if you want to put your company in the best light when raising capital, it’s important to understand your target investors so you can tailor your pitch.

Business Valuation Myth #2: A good valuation provides a precise estimate of value.

In some sense, investors are not that interested in precise value. Think about it. What does the value of a company today tell you? This is a measure of what the company has done in the past. But investors are really interested in what the company will do in the future. So, the current value need not be precise to determine whether the business is a smart investment.

In fact, while this is somewhat dependent on industry, it’s arguable that the ROI is greatest when the business valuation is least precise. This could be one of the lessons learned from analyzing the VC industry in Silicon Valley.

Look at Uber, for instance, the world’s most valuable VC-backed company, with an estimated valuation of $62 billion. It’s burning through cash, losing between $500 million and $1.5 billion per quarter on a run-rate basis since early 2017. Yet the company still raised a $1.25 billion Series G led by SoftBank earlier this year, according to the PitchBook Platform.

Business Valuation Myth #3: The more quantitative the model, the better the valuation.

There are a few different schools of thought here, but often the more numbers contained in the model, the more questions investors will have. The best valuation is the one that makes sense and is clear enough to be pressure tested by investors. So beware of overly complex quantitative models and numbers that need a lot of explaining.

As you can see, business valuation for private companies is full of assumptions, educated guesses, and projections based on industry averages. With the lack of transparency, it’s often difficult for investors and analysts to place a reliable value on privately-held companies. However, this is really not much different from other aspects of business. Whether you’re a business owner considering how to raise capital or an investor looking to take a chance by getting in on the ground floor of the next big dog, business is all about taking calculated risks.

At Audacia Strategies, we love to help companies in all stages. You choose the next calculated risk and we’ll be there to support you in making bold moves confidently. Business valuation is not for the faint of heart. Get the right team on your side!

Photo credit: pressmaster / 123RF Stock Photo