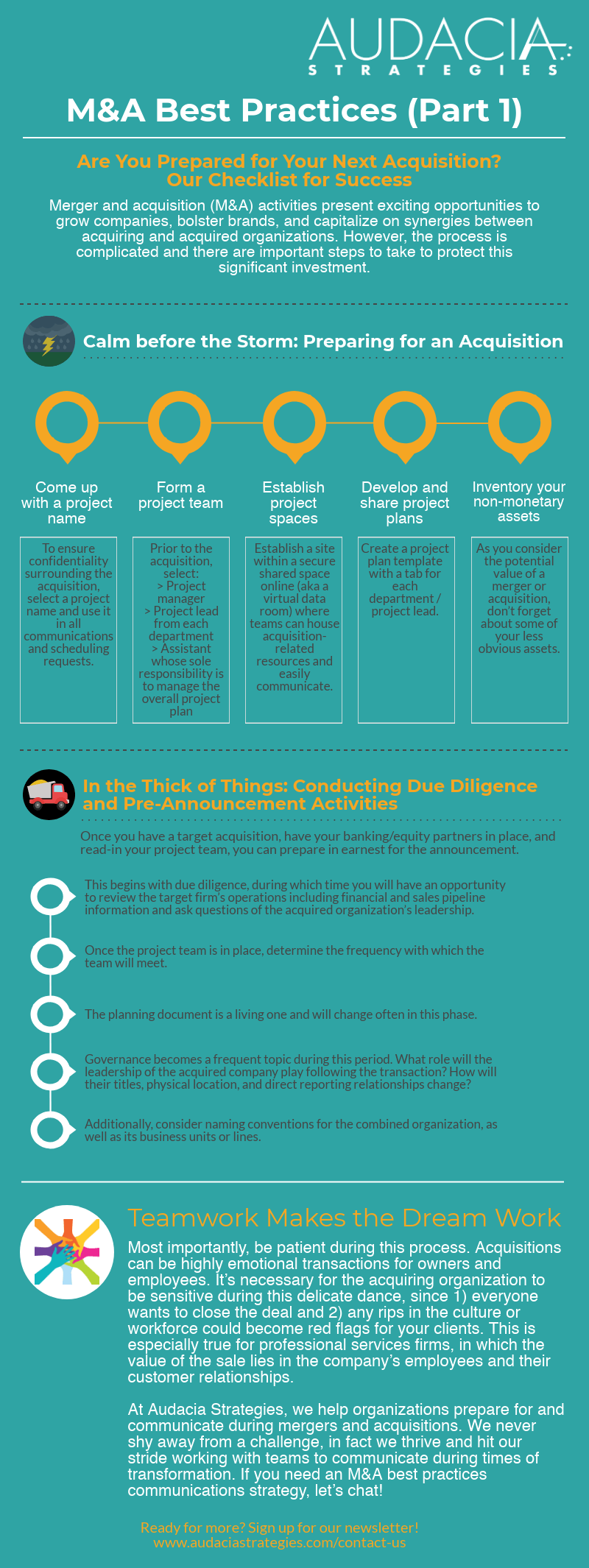

Smart Planning for Executive Transitions: When You See It Coming (Part 1)

Transitions, including executive transitions, are high stakes for companies for obvious reasons. They bring about logistical, bureaucratic, professional, and emotional challenges for everyone involved. That’s why we’ve created a two-part Executive Transition Series to help you out during seasons of change in your company.

Executives can be a powerful retention mechanism, or the reason people leave. Consider the old adage, people quit bosses, not jobs. Alternatively, sometimes employees come to a company to work with a particular leader. What happens when that leader leaves? And what about when veteran employees have worked with the same leader for multiple years, and a new leader radically changes the culture? These are tough questions, and not ones you can sweep under the rug.

The key for dealing with executive transitions is communication. It’s important to tailor your strategy to the kind of transition you’re facing. On the one hand, you might be facing a planned transition—one that’s been on the horizon for months or years. On the other hand, you might have a leader—maybe one who hasn’t even been around very long—give two weeks notice. These are two very different situations, and having a strategic communications plan can help you make it through either one.

In this two-part series, we’ll consider both situations. First, we’ll consider some tips for handling a planned transition.

4 Tips for Planned Transitions

Executive transition is a specialty of ours here at Audacia Strategies. Let me share one of my favorite engagements and biggest client wins when supporting a client through a planned transition. Recently, Audacia was brought on board to help with an executive transition in a software company. The outgoing senior executive was the founder of the company and also an avid, talented guitarist. A low key rockstar, if you will. The company culture was centered around music: leadership documents were full of music analogies, guitars were given as gifts, leaders put their favorite song in their website bio–you get the picture.

The leader planned his exit and helped to identify a new CEO. The new CEO was brilliant—he had run billion-dollar organizations and grew up playing chess blind-folded! While this new CEO was a great fit to guide the company to its next phase of growth, he was different from the founder-CEO. An executive transition is one thing, but the reality is that the company was also about to undergo a cultural transition.

How do you manage the exit in a case like this? Here’s the playbook we advised.

1. Storytelling

As long as people have been around, they have connected over stories. We made space for the outgoing CEO to share his story, and time to celebrate his work with the company. Just like a graduation or retirement party, this allows for closure and creates appropriate professional space for processing the (big) feelings that come with transitions.

2. Getting to know the new leader

In addition to telling the story of the outgoing CEO’s time, we worked with the incoming CEO to help him identify and share his story. This humanized an ultra-smart leader and gave employees a chance to get to know him and understand his priorities and what makes him tick.

We also advised on creating plenty of opportunities and multiple channels to engage with the CEO and ask questions. Unanswered questions can leave employees feeling ungrounded and many may be too intimidated to ask the hard (or even simple!) questions.

We always advise to be as open as possible and provide opportunities for interaction in multiple formats (in-person, online, large group, small group, 1-to-1). Transparency and accessibility are key for maintaining and building trust.

3. Working with the team

The logistics and bureaucracy involved in a transition are not to be underestimated; however, it’s also important to work closely with the team. Share the transition plan, let your executive team know what is coming and let them weigh in on what they and their teams need. And, practically speaking, set expectations about which responsibilities will be redistributed, who will be responsible for training whom, and so on. Executives have questions too–give them time to process the transition and bring their questions to the new executives or trusted confidants.

4. Mind your communications

We trade a lot in written word, scripts, and talking points. Emails and other written messages are important artifacts that preserve institutional memory long after the transition. Because everyone can look back and see where leaders followed through and where they didn’t, it’s important to be consistent across multiple mediums (video intros of a new CEO, webcast town hall, in-person meet and greets, welcome letter, and so on).

Perhaps even more importantly, organizations should make sure messaging is consistent across informal communications as well. During times of transition, employees will first bring their worries and questions to direct supervisors and peers. The executive team and their team needs to be on the same page so they’re ready to help their teams navigate organizational changes. During times change most employees and customers will turn to their line manager or customer success contact for reassurance, make sure these critical team members have the information, resources, and support they need to succeed.

Concluding Thoughts

Planned transitions are admittedly easier than unplanned transitions; however, planned transitions can still be destabilizing to company culture. At worst, transitions can result in employee turnover, loss of trust, lost business momentum, and a decline in workplace climate if you don’t go in with a strategy. It’s important to keep in mind both the emotional and logistical challenges of executive transitions.

We often think about corporations as faceless entities, but in moments of transition, we are reminded that corporations are made up of people who have hearts and minds. The more you share your story honestly, transparently, and thoughtfully, the more you can weather this season of transition while building long-term trust and continuing to achieve your company goals.

If you don’t have the luxury of a planned transition and are facing an imminent unplanned transition, read the next part of our two-part series where we’ll discuss tips for handling an unplanned executive transition.

If you’re facing a transition—planned or unplanned—and you’re trying to find the right strategy, Audacia has you covered. Reach out to us here to schedule a consultation.

Photo Credit: Black Male And White Female Business Associates Shaking Hands In Hallway by Flamingo Images from NounProject.com